How to Refinance Your Mortgage in Ontario to Consolidate Debt (2025 Guide)

Juggling payments for credit cards, car loans, and your mortgage can be overwhelming and costly. This guide explains how homeowners in Whitby and across Ontario can use a mortgage refinance as a powerful tool to consolidate high-interest debt into one simpler, lower-interest payment. Discover the step-by-step process, see a case study on improving cash flow, and learn the key considerations to decide if this strategic move is right for you.

Lokesh Tuli

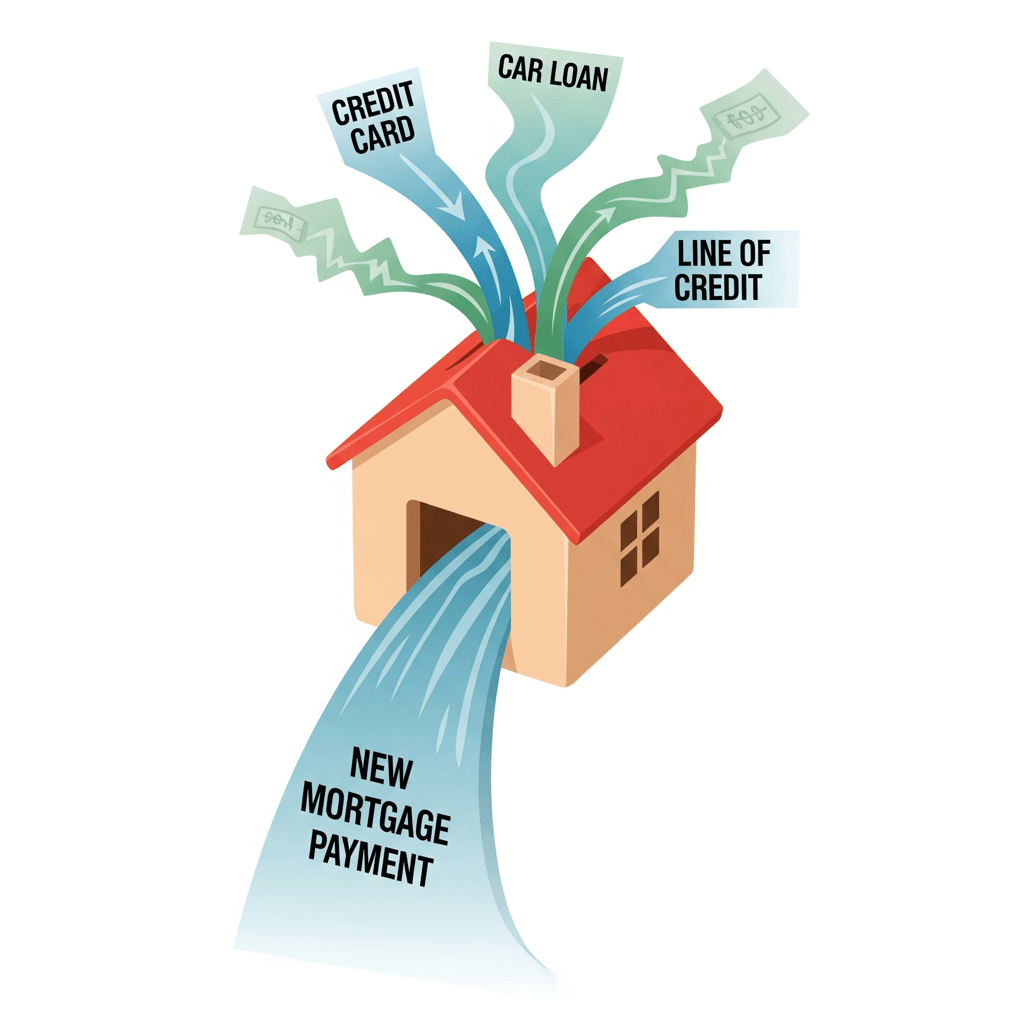

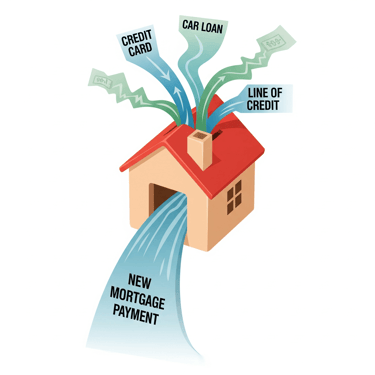

Are you juggling multiple monthly payments? Do you feel like you’re on a treadmill, making payments on high-interest credit cards and loans but never getting ahead? This is a common source of financial stress for many homeowners in Ontario. The good news is, the solution to improving your cash flow might be right under your roof: your home equity.

As a Mortgage Planner and Strategist, I help homeowners explore their options beyond a simple renewal. One of the most powerful strategies is a mortgage refinance to consolidate debt. This guide will explain how you can use this tool to simplify your finances, reduce your interest costs, and get back in control.

What is a Mortgage Refinance?

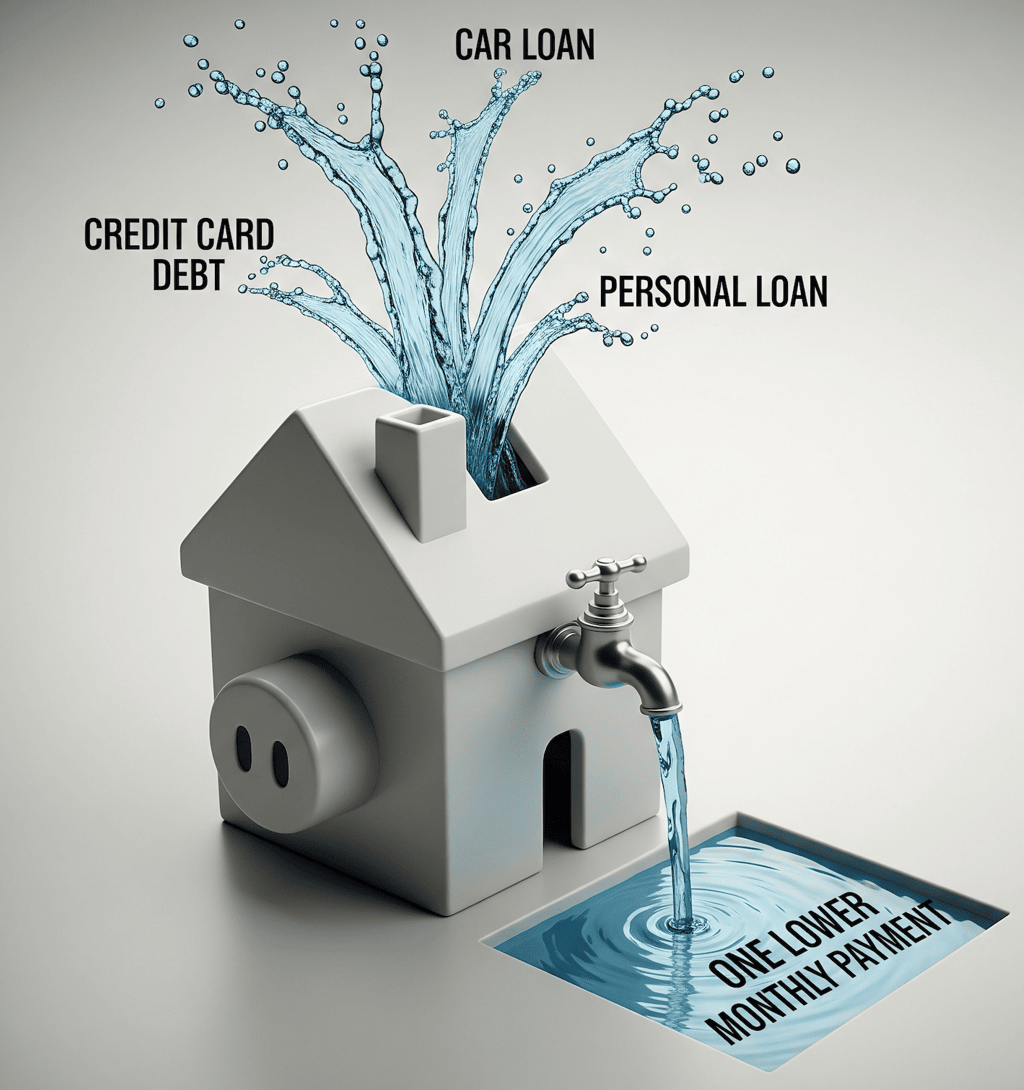

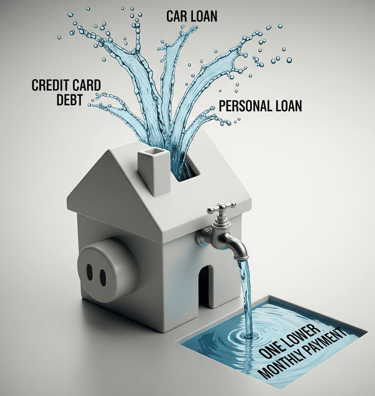

A mortgage refinance simply means replacing your existing mortgage with a new, larger one. You use the new mortgage to pay off the old one, and the extra funds—the equity you’ve built in your home—are used to pay off other, higher-interest debts.

This is different from a renewal, where you just renew your existing mortgage balance for a new term. It is also different from a second mortgage, which is an entirely separate loan in addition to your primary one. A refinance combines everything into a single, simple mortgage payment.

The Step-by-Step Process to Consolidate Debt

Refinancing can seem complex, but it breaks down into a few clear steps:

Step 1: Assess Your Financial Picture The first step is a confidential review of your finances. We’ll look at:

The current value of your home.

Your outstanding mortgage balance.

A list of all the debts you want to consolidate (e.g., credit cards, car loans, lines of credit) and their respective interest rates.

Step 2: Determine Your Available Equity In Canada, you can typically borrow up to 80% of your home's appraised value. We calculate your available equity to see how much room you have. For example, on a $800,000 home, you could potentially borrow up to $640,000. If your current mortgage is $400,000, you may have access to $240,000 to consolidate debts.

Step 3: The Application & Approval Process Applying for a refinance is similar to applying for a new mortgage. We submit an application to a lender who can offer a competitive rate. This process includes verifying your income and getting a new appraisal on your property to confirm its current market value.

Step 4: Paying Off Your Debts & Simplifying Your Life Once your refinance is approved, the process is handled by your lawyer. The new mortgage funds are used to pay off the old mortgage and then sent directly to your creditors to eliminate your high-interest debts. The result? You are left with one single mortgage payment, often at a much lower interest rate than your previous debts.

Frequently Asked Questions (FAQ)

1. Is it difficult to switch lenders at renewal? Not at all. When you work with a mortgage professional, the process is simple and streamlined. We handle the paperwork and communication to make the switch seamless.

2. Will shopping for a new mortgage hurt my credit score? When done correctly, no. A single credit inquiry from a mortgage professional allows us to check with multiple lenders. This is treated as a single "hard inquiry" and has a minimal, temporary impact on your score, unlike applying to multiple lenders yourself over several weeks.

3. What’s the difference between renewing and refinancing? A renewal is simply renewing your existing mortgage balance with a new term and rate (either with your current lender or a new one). A refinance involves changing the terms of your mortgage, often by borrowing more than you currently owe to access equity or consolidate debt. We can discuss which is right for you.

Case Study: How Refinancing Helped a Whitby Family

Consider a hypothetical family in Whitby with the following monthly payments:

Current Mortgage: $2,200

Car Loan (at 7%): $550

Credit Card Debt (at 21%): $450

Total Monthly Payments: $3,200

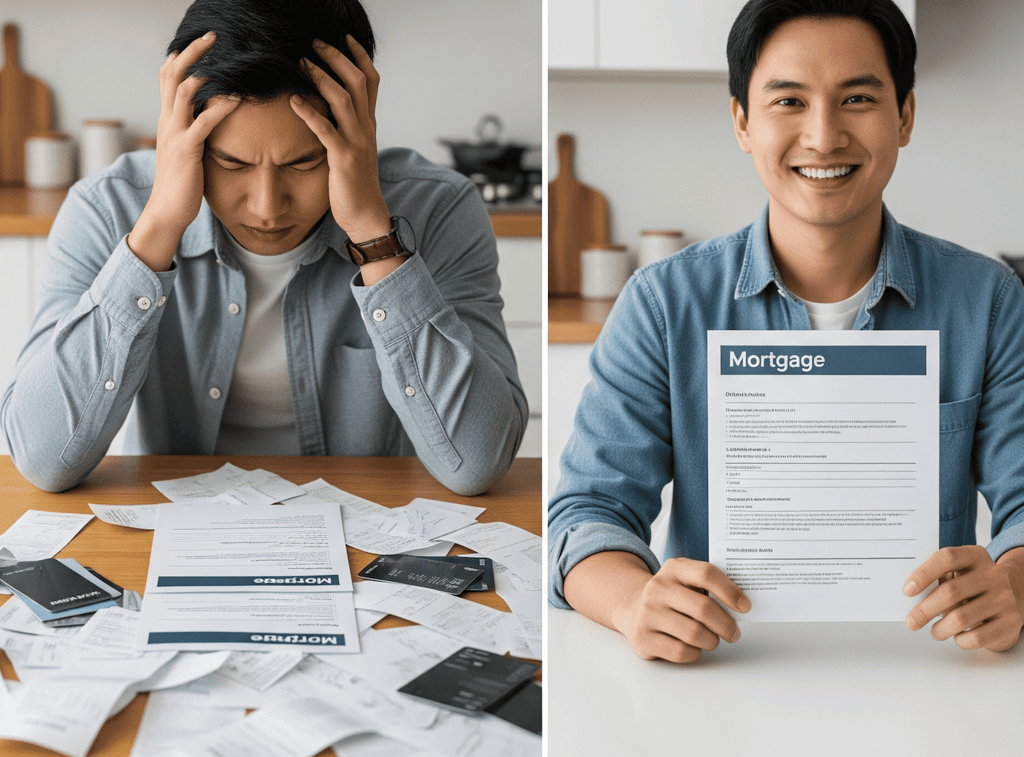

By refinancing their mortgage, they were able to roll all three debts into one new mortgage. Their new single mortgage payment became approximately $2,750. In this example, they improved their monthly cash flow by $450 and are now paying off their debt at a much lower mortgage interest rate.

Is a Debt Consolidation Refinance Right for You?

This is a powerful strategy, but it requires careful consideration.

It might be a great option if:

You are struggling with high-interest debt from credit cards or unsecured loans.

You have a disciplined plan to manage your finances moving forward.

You have built up sufficient equity in your home.

It may not be the right fit if:

You would face very large penalties for breaking your current mortgage term early.

It is being used as a temporary solution for ongoing overspending habits.

How a Mortgage Strategist Can Create Your Smart Plan

My role is to help you analyze your unique situation and create a smart plan to eliminate high-interest credit card & loan debt. I will help you weigh the pros and cons, calculate the potential savings, and simplify the entire process with step-by-step support from start to finish.

Feeling the pressure of high-interest debt? You have options. A confidential, no-obligation consultation can show you what's possible.

Stop Juggling Debt & Turn Multiple Payments Into One Simple Solution?

In a free, 15-minute confidential chat, we'll calculate exactly how much you could save by consolidating high-interest debt into a single, lower-rate mortgage payment.

Schedule your complimentary strategy session below and let's get you back in control.