How Much Down Payment Do You Need in Ontario? (Your 2025 First-Time Buyer Guide)

Planning to buy your first home in Whitby or across Ontario but feeling confused about the down payment? This simple 2025 guide breaks down the exact minimum down payment percentages, explains mortgage default insurance, and details other essential closing costs you need to budget for. Stop feeling overwhelmed and start planning your purchase with a clear understanding of the numbers involved.

Lokesh Tuli

Congratulations! You’re thinking about buying your first home in Ontario. It's an exciting and life-changing goal. But before you start Browse listings in Whitby or across the GTA, the first question on your mind is likely the biggest: "How much money do I actually need for a down payment?"

Feeling confused by all the numbers and rules is completely normal. As a Mortgage Planner & Strategist, my goal is to simplify this process for you. This guide will break down the exact down payment rules in Ontario, explain where the money can come from, and show you how to get started on your homeownership journey with confidence.

The Minimum Down Payment Rules in Ontario

In Canada, the minimum down payment you need depends on the purchase price of the home. It’s a tiered system, not a single flat percentage.

Here is the official breakdown for homes under $1 million:

For homes up to $500,000: You need a minimum down payment of 5%.

For homes between $500,000 and $999,999: You need 5% on the first $500,000, plus 10% on the portion of the price above $500,000.

Let's look at two common examples:

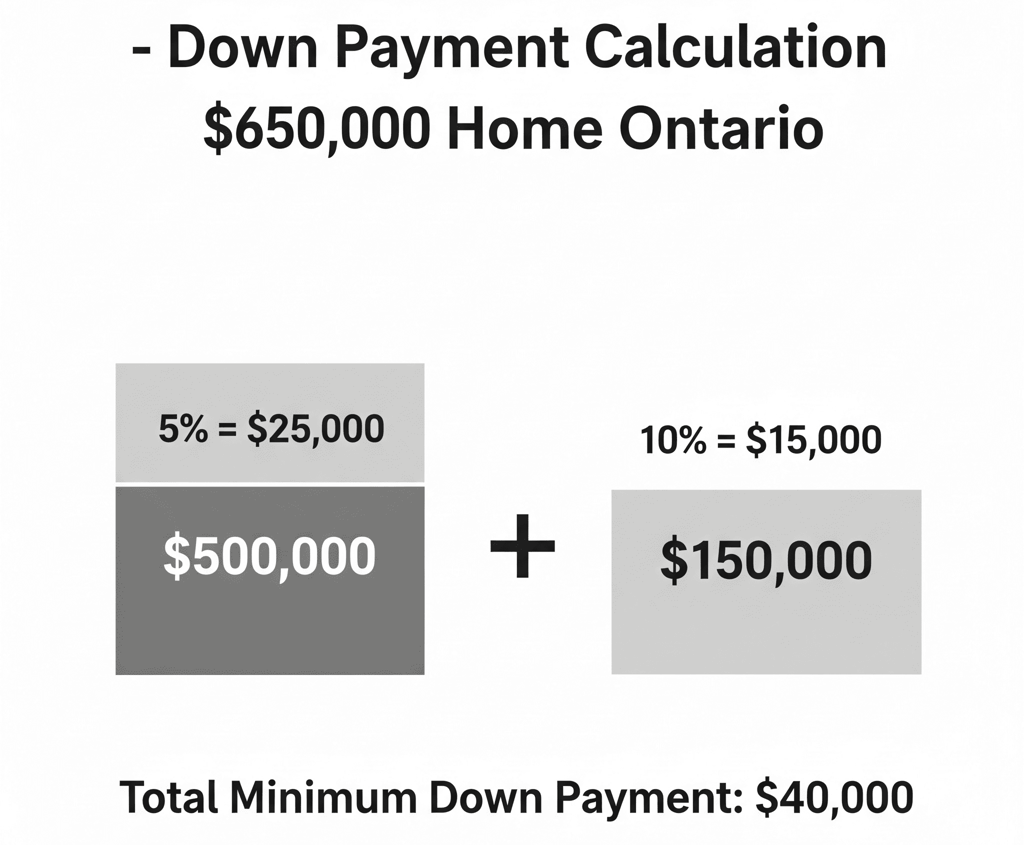

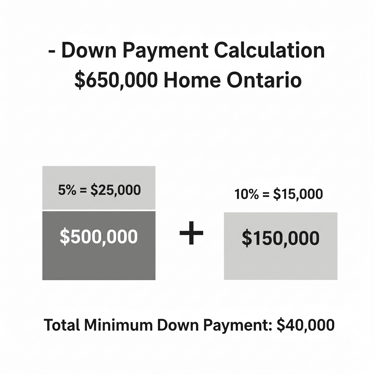

Example 1: A $650,000 Home

5% on the first $500,000 = $25,000

10% on the remaining $150,000 = $15,000

Total Minimum Down Payment: $40,000

Example 2: For Homes $1,000,000 or more For any property with a purchase price of $1 million or more, the minimum down payment is 20% of the total purchase price.

What is Mortgage Default Insurance (CMHC Insurance)?

This is a crucial concept to understand. If your down payment is less than 20% of the purchase price, you are legally required to have mortgage default insurance. This is often called CMHC insurance (named after the Canada Mortgage and Housing Corporation, one of its main providers).

This insurance doesn’t protect you; it protects the lender in case you are unable to make your mortgage payments. The cost of this insurance is a percentage of your mortgage amount and is usually added directly to your total mortgage balance, so you don’t pay it all in one lump sum. Putting 20% or more down allows you to avoid this extra cost.

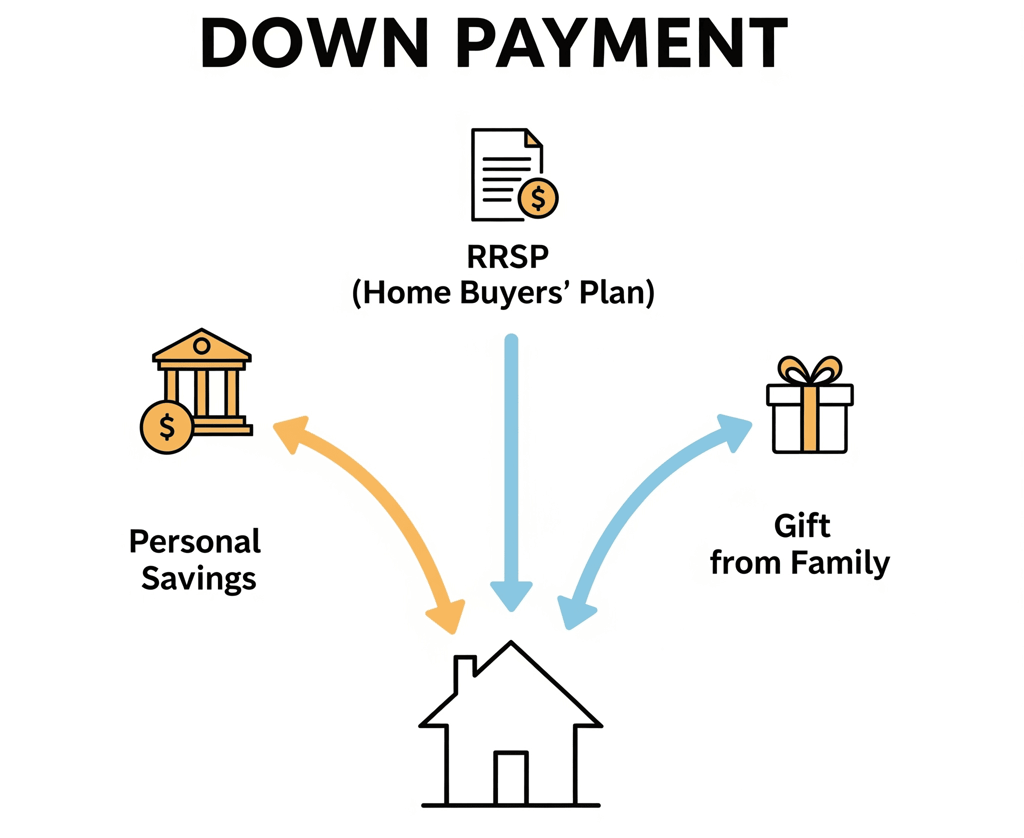

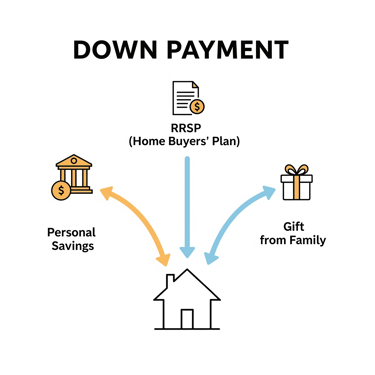

Where Can Your Down Payment Come From?

Lenders need to see that your down payment comes from legitimate sources. The most common acceptable sources include:

Personal Savings: Money you have saved in your bank accounts (chequing, savings, TFSA, GICs).

RRSP (Home Buyers' Plan): First-time buyers can withdraw up to $35,000 tax-free from their RRSPs to use towards a down payment.

A Gift from an Immediate Family Member: A parent or close relative can gift you money for your down payment. A "gift letter" signed by them is required to prove it is not a loan.

Beyond the Down Payment: Don't Forget Closing Costs!

This is a critical tip that a good Mortgage Planner will always give you. Your down payment is not the only cash you’ll need. Closing costs are separate expenses due on closing day. These can include:

Ontario Land Transfer Tax

Lawyer/Notary Fees

Title Insurance

Property Appraisal Fees

As a general rule, you should budget an additional 1.5% to 4% of the home's purchase price for closing costs.

How a Mortgage Planner Helps You Succeed

Navigating these numbers and rules is the first step. The next is getting an "Iron-Clad Pre-Approval" so you can shop with confidence. My role is to simplify this entire process with step-by-step support. I work with dozens of lenders, unlocking mortgage options the banks don't advertise to find a solution that fits your unique financial picture.

Ready to find out what you can afford? Let's create a clear plan for your first home purchase.

Let's Create Your Personalized Down Payment Plan.

The numbers in this guide are the first step. The next step is applying them to your unique situation.

In a complimentary 15-minute call, we'll calculate exactly what you need for a down payment and closing costs, and create a clear roadmap for your first home purchase

Schedule a free, no-obligation call below to get pre-approved.